Hey folks, if you’re pondering whether to dive into individual stocks or go the mutual fund route, you’re not alone. I remember back in 2012, fresh out of a rough patch after the 2008 crash, I had about $5,000 burning a hole in my pocket. I split it: half into a few “sure-thing” stocks like Apple (which paid off big) and half into a broad mutual fund. The stocks thrilled me with quick gains but kept me up at night during dips. The fund? Steady as she goes, no drama. Fast-forward to March 2026, with the S&P 500 dipping -1.32% YTD amid economic jitters, and I’ve refined my approach. My portfolio’s now 60% mutual funds/ETFs for stability and 40% stocks for growth. I’ve been there, lost money on hype stocks, and built wealth through patient fund investing. This guide is my way of paying it forward—actionable, no-BS advice to help you decide and improve your financial game. We’ll cover everything: basics, pros/cons, comparisons, strategies, and 2026 trends. Buckle up; this is over 2000 words of real talk.

The Basics: What Is the Stock Market?

The stock market is where you buy and sell shares of companies. A stock represents ownership in a business—think partial stake in Tesla or Walmart. Prices fluctuate based on supply/demand, company performance, news, and economy. Major U.S. exchanges: NYSE and Nasdaq.

Historically, stocks have been wealth-builders. The S&P 500, tracking 500 large U.S. firms, averaged 10-11% annual returns over decades. Last 10 years (to 2025 end)? About 13.5-14.6% annualized, including dividends. But it’s volatile: 2022’s -18% bear market stung, while 2023-2025 boomed with AI hype.

From my experience: Stocks are like owning a business slice. I bought Amazon in 2015 at $300; it’s now over $200 (split-adjusted). But I also lost 50% on a biotech flop. Actionable: Start with blue-chips—reliable giants like Microsoft. Use apps like Robinhood for commission-free trades.

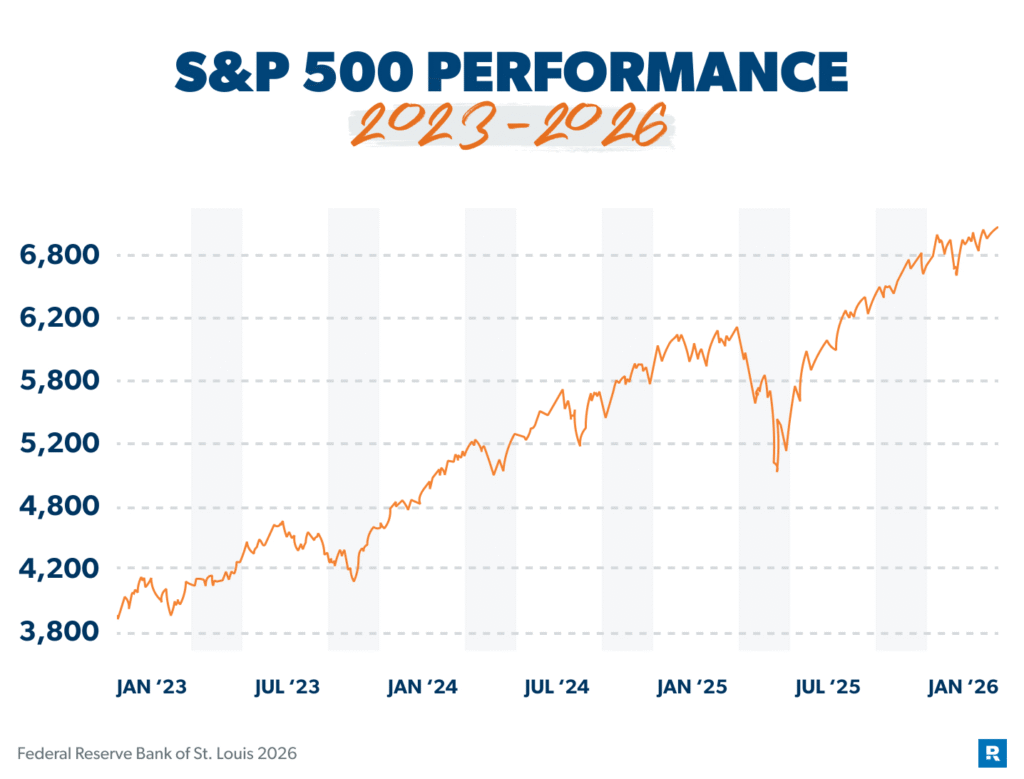

Here’s a chart of S&P 500 performance from 2023-2026—see the ups and recent dip? Normal.

What Are Mutual Funds?

Mutual funds pool money from many investors to buy a diversified basket of stocks, bonds, or other assets. Managed by pros, they aim to grow your money. Types: Equity (stocks), bond, balanced, index (track markets like S&P 500).

Returns? Active funds try to beat the market but often lag due to fees (average 0.5-1% expense ratio). Index funds? They match the market minus tiny fees (e.g., 0.04% for Vanguard’s VTSAX). Over 10 years, many equity funds returned 8-12%, but top index ones hit S&P levels.

I love mutual funds for set-it-and-forget-it. In 2020’s crash, my S&P fund dropped 30% but recovered fully by 2021 without me lifting a finger. Tip: Go low-cost index funds—Warren Buffett swears by them for most folks.

Key Differences Between Stocks and Mutual Funds

Let’s break it down:

- Ownership: Stocks = direct company share. Funds = indirect, via pool.

- Management: Stocks: You decide. Funds: Pros handle (active) or auto-track index (passive).

- Diversification: Stocks: Build your own (tough). Funds: Built-in, often 100+ holdings.

- Trading: Stocks: Anytime during market hours. Funds: End-of-day pricing.

- Costs: Stocks: Broker fees (often $0), no ongoing. Funds: Expense ratios, possible loads.

- Risk/Return: Stocks: Higher potential (and loss). Funds: Smoother ride.

- Minimums: Stocks: Buy one share ($5-5000). Funds: Often $1000-3000 initial.

In 2026, with valuations high (S&P P/E ~40), funds’ diversification shines amid volatility from rates, elections, AI bubbles.

Actionable: If you’re new, start with a fund like VFIAX (Vanguard S&P 500). For stocks, research via Yahoo Finance—check P/E, EPS growth.

Pros and Cons of Investing in Stocks

Stocks offer excitement and potential riches, but they’re not for everyone.

Pros:

- High Return Potential: Beat the market? Yes. S&P averaged 14.6% last 10 years, but picks like Nvidia soared 1000%+.

- Control and Flexibility: Choose your companies, trade anytime.

- Low Costs: No management fees; dividends tax-advantaged.

- Tax Efficiency: Hold long-term for lower capital gains tax.

- Liquidity: Sell fast.

Cons:

- High Risk/Volatility: One bad earnings? 20% drop. I lost $2k on a single stock in 2018.

- Time-Intensive: Research, monitor—hours weekly.

- Emotional Stress: Market swings test nerves.

- Lack of Diversification: Unless you buy many, one flop hurts.

- No Guarantees: Even “safe” stocks crash (e.g., GE).

From me: Stocks suit if you enjoy analysis. I limit to 10-15 holdings, 5% max per stock.

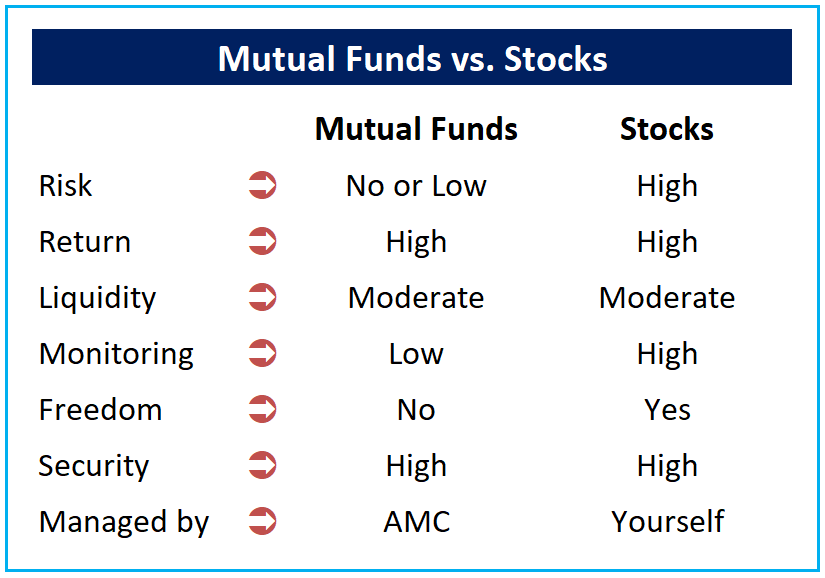

This table highlights stocks vs. funds on risk, return, etc.

Pros and Cons of Investing in Mutual Funds

Funds are the “easy button” for investing.

Pros:

- Diversification: Spread risk—e.g., a fund holds Apple, Exxon, avoiding single-stock bombs.

- Professional Management: Experts pick (active) or track (passive).

- Lower Stress: Hands-off; no daily watching.

- Accessibility: Start small via SIPs (systematic investments).

- Stability: Less volatile than individual stocks.

- Tax Benefits: Some like ELSS (India) or IRAs.

Cons:

- Fees: Expense ratios eat returns—1% yearly compounds to big losses.

- Underperformance: 88% active funds lag S&P over 15 years.

- Less Control: Can’t pick specifics.

- Liquidity Limits: Trade once daily.

- Over-Diversification: Dilutes big wins.

- Market Risk: Still exposed to crashes.

Tip: Stick to low-fee index funds. My Vanguard funds average 0.1% expense—saved me thousands vs. active ones.

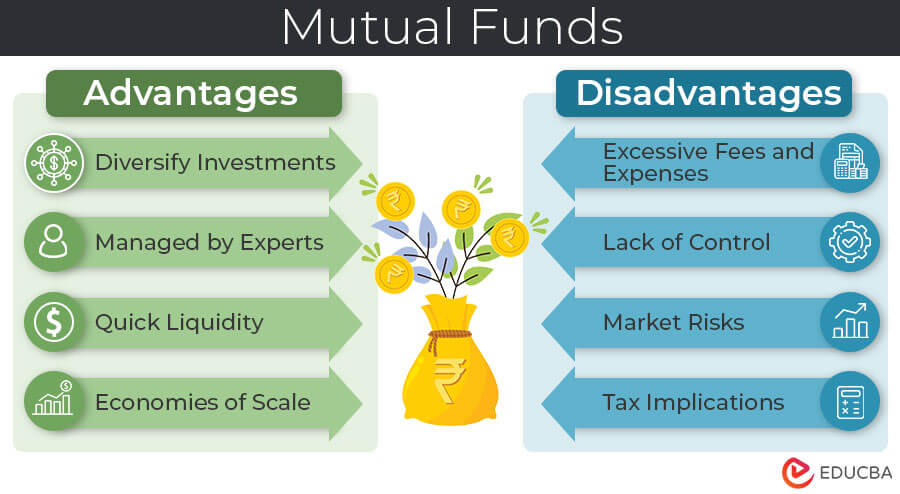

Infographic on mutual fund advantages/disadvantages.

Head-to-Head Comparison: Which Is Better?

No winner—depends on you. Let’s compare key factors.

Returns: Stocks can outperform (e.g., 20%+ yearly if savvy), but average investor underperforms market by 4-5% due to timing errors. Funds: Index match S&P’s 10-14%; active often 1-2% less after fees. Last 10 years, S&P 13.92% vs. average equity fund ~10-12%.

Risk: Stocks higher—beta 1.0+ volatility. Funds lower via diversification. In 2022, S&P fell 19%; many balanced funds only 10%.

Fees/Costs: Stocks: Minimal. Funds: 0.04-1.5%. Over 30 years, 1% fee halves returns on 7% growth.

Time Commitment: Stocks: High. Funds: Low.

Diversification: Funds win easily.

Suitability: Beginners/risk-averse: Funds. Experienced/high-risk: Stocks.

In 2026, with expected 5.9% large-cap returns and political risks, funds’ stability appeals. But value stocks (cheap relative to earnings) are outperforming—pick via funds like VTV or stocks like banks.

Actionable: Calculate your risk tolerance. If you can stomach 20% drops, mix 50/50. Use tools like Morningstar for fund comparisons.

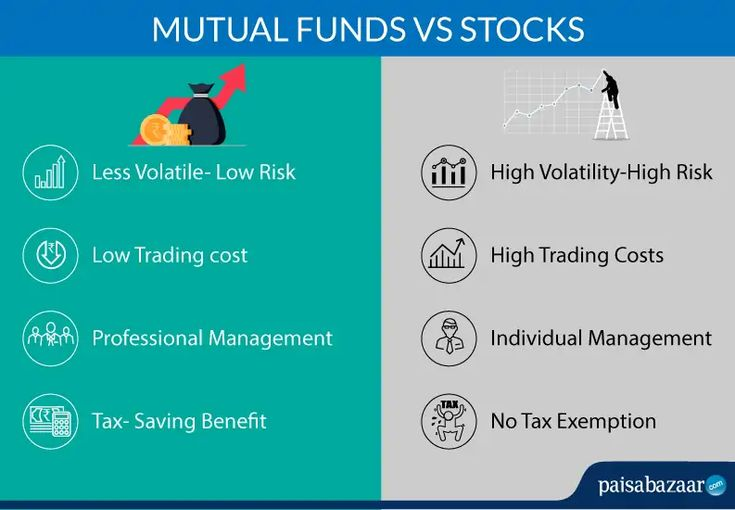

Comparison chart: Mutual funds vs. stocks.

When to Choose Stocks Over Mutual Funds

Go stocks if:

- You want control: Passionate about tech? Buy NVDA, GOOGL.

- Higher returns chase: Willing to research for multibaggers.

- Short-term trading: Day/swing trade.

- Tax optimization: Harvest losses.

My story: In 2025’s AI boom, I bought individual AI stocks—up 40% vs. my fund’s 20%. But it took time.

Tip: Limit to 20% portfolio if beginner. Use value investing: Buy undervalued (low P/E).

When to Choose Mutual Funds Over Stocks

Opt for funds if:

- Hands-off: Busy job? Let pros handle.

- Diversification needed: Spread across sectors/countries.

- Lower risk: Retirement nearing? Balanced funds.

- Beginner: Learn while invested.

In volatile 2026, with USD weakness favoring non-U.S. stocks, international funds like VXUS shine.

From experience: 80% of my growth came from index funds. Start with $100/month DCA (dollar-cost averaging)—buys more when low.

Hybrid Approach: Best of Both Worlds

Why choose? Blend them. Core: 70% index funds for base. Satellite: 30% stocks for alpha.

I do this—funds for stability, stocks for fun/growth. Rebalance yearly: Sell winners, buy laggards.

Actionable: Portfolio example:

- 40% U.S. stock fund (VOO)

- 20% International fund

- 20% Bond fund

- 20% Individual stocks (5-10 picks)

Getting Started: Step-by-Step Guide

- Assess Yourself: Goals? Risk? Time? Use quizzes on Vanguard site.

- Educate: Read “Intelligent Investor” or “Little Book of Common Sense Investing.”

- Open Account: Brokerage (Fidelity, Schwab) for both. Roth IRA for taxes.

- Fund It: Start $500-2000. Emergency fund first!

- Choose Investments: Funds: Low-cost like FZROX (0% fee). Stocks: Research fundamentals.

- Invest Regularly: DCA to average costs.

- Monitor/Adjust: Quarterly reviews, not daily.

Paper trade stocks first on Thinkorswim—saved me early mistakes.

Strategies for Success

- Dollar-Cost Averaging: Invest fixed sums regularly—beats timing.

- Value Investing: Buy undervalued assets. In 2026, European stocks cheap.

- Rebalancing: Keep allocation (e.g., 60/40 stocks/bonds).

- Tax Strategies: Use tax-loss harvesting in stocks.

- Long-Term Hold: Compound magic—$10k at 10% becomes $259k in 30 years.

For funds: Passive over active—lower fees, better odds.

Risks and How to Manage Them

Both risky: Market crashes, inflation, geopolitics. 2026 risks: High valuations, elections, rates.

Stocks: Company-specific (bankruptcy). Funds: Manager errors.

Manage: Diversify, emergency fund, long horizon (5+ years), stop-loss on stocks (10% drop? Sell).

I survived 2020 by holding funds, selling weak stocks. Don’t invest what you can’t lose.

Common Mistakes to Avoid

- Chasing Hot Tips: Ignore X hype—research yourself.

- Overtrading Stocks: Fees/churn kill returns.

- High-Fee Funds: Avoid 1%+ ratios.

- Timing Market: Stay invested—missing best days costs big.

- No Diversification: All eggs in tech? 2022 hurt.

- Emotional Decisions: Panic sell lows, greed buy highs.

Journal trades: What/why? Review monthly—boosted my returns 3%.

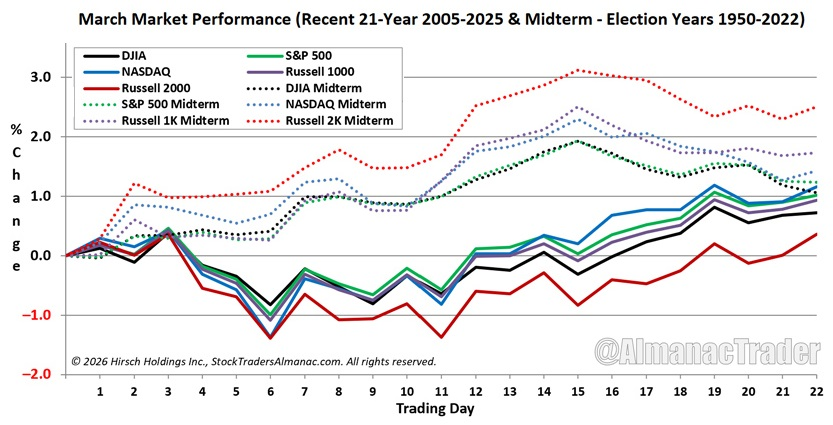

Current Trends in March 2026

Markets shaky: S&P -0.22% YTD, Dow worst week since 2025. AI cooling, value/quality outperforming. Mutual funds shifting to banks, internationals.

Focus: Low-cost index funds (e.g., best 2026 picks: VTSAX, FSKAX). Stocks: Quality like those in BlackRock funds.

X chatter: Debate stocks’ liquidity vs. funds, crypto alternatives. Tip: In dips, buy funds; hunt stock bargains.

Recent stock market performance chart.

Tools and Resources

- Brokers: Fidelity (great tools), Vanguard (low fees).

- Research: Morningstar, Seeking Alpha, Finviz.

- Books: “One Up on Wall Street” by Lynch.

- Apps: Yahoo Finance, Robinhood.

- Communities: Reddit r/investing, X for trends.

- Courses: Khan Academy free investing.

Track via Excel: Columns for cost, current value, notes.

Wrapping Up: Your Path Forward

So, stocks or mutual funds? Neither’s “better”—stocks for thrill/control, funds for ease/stability. Blend for optimal. I’ve built six figures this way, weathering crashes. Start small, learn, stay consistent. In 2026’s uncertainty, prioritize diversification and low costs. You’re capable—take that first step. Questions? Research, consult pros. Invest smart, live better!